Now Reading: JPMorgan Now Accepts Crypto as Collateral: Is Traditional Finance Changing for Good?

-

01

JPMorgan Now Accepts Crypto as Collateral: Is Traditional Finance Changing for Good?

JPMorgan Now Accepts Crypto as Collateral: Is Traditional Finance Changing for Good?

JPMorgan, one of the world’s biggest banks, has taken a bold step: it’s now allowing clients to borrow money using cryptocurrencies as collateral. This shift, while happening in the US, sends ripples globally—including to India, where crypto adoption is rising fast, especially in Tier 2 cities. Is this a new beginning for crypto legitimacy in finance, or just a calculated experiment? Let’s unpack what this move really means.

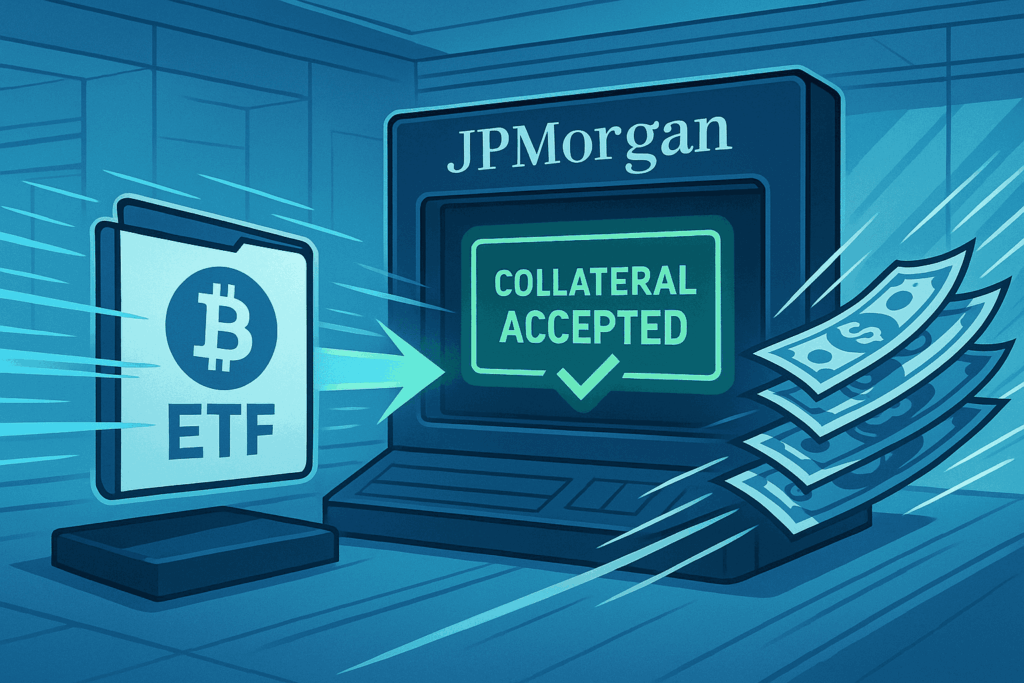

What Exactly Is JPMorgan Doing?

JPMorgan isn’t giving loans in crypto. Instead, it’s accepting crypto like Bitcoin or Ethereum as security against cash loans. So if you hold a large amount of crypto, you don’t need to sell it—you can use it as a guarantee and still get liquidity.

This is similar to taking a gold loan in India. You hold on to your asset while accessing funds against its value.

Why This Move Matters Globally

When a bank like JPMorgan enters the crypto lending space, it sends a strong signal: digital assets are no longer just speculative bets—they’re becoming part of mainstream finance. This could push other banks and financial institutions to explore similar models.

It also marks a shift in how the financial world views crypto. From being labeled ‘risky’ or ‘illegal’ by traditional institutions, crypto is slowly gaining recognition as a legitimate store of value.

India’s Crypto Scene: Could This Happen Here?

Crypto investments are no longer limited to metro cities. In places like Nagpur, Indore, and Surat, more people—especially young professionals—are investing in digital assets. But Indian banks haven’t yet warmed up to the idea of accepting crypto as collateral.

This is mostly because of regulatory uncertainty. The Reserve Bank of India remains cautious, and crypto’s legal status is still in limbo. Until clear frameworks are in place, banks here are unlikely to follow JPMorgan’s lead.

The Risks Involved

Accepting crypto as collateral isn’t without risk. Prices fluctuate wildly. If the value of the collateral drops below a certain point, the lender could face losses. That’s why such loans usually include “margin calls”—if prices fall, the borrower has to top up the collateral or risk liquidation.

For Indian regulators, this is a key concern. Without strong guidelines, allowing crypto-based loans could expose both banks and borrowers to unnecessary risk.

But It’s Also an Opportunity

If done right, crypto lending can help improve liquidity in the market. For small businesses or individuals holding digital assets, it offers access to cash without selling their investments.

It also opens up new financial tools for India’s growing Web3 ecosystem—developers, creators, and startups could benefit from a system where crypto is treated like any other financial asset.

Conclusion

JPMorgan’s move doesn’t mean Indian banks will start accepting crypto collateral overnight. But it does set the tone. The more global institutions start treating crypto seriously, the harder it becomes for Indian regulators to ignore its potential. The question isn’t whether crypto will enter mainstream finance—it’s how and when India decides to join the table